Asia

Region

ASIA

Asia, led by China and India, installed far more clean energy capacity in 2015 than the other two regions surveyed by Climatescope. China is of course at the heart of this and it posted another record year despite being in the midst of far-reaching power sector reforms. Taking a cue from Germany and others, China now plans to transition away from fixed tariff-based mechanisms toward market-based incentives for renewables. This follows the trend seen in India where auctions have allowed the procurement of new solar PV capacity at record-low prices.

The growth of renewables has, however, not been free of challenges in China and India. Both are grappling with integrating this new, clean, but variable resource. Each are also confronting costs associated with subsidy programmes.

Other Climatescope Asia countries were hardly idle in 2015 though their performances were overshadowed by the region’s two giants. New and important steps were taken to improve market conditions for renewables in a number of these countries, such as measures to improve access to capital for developers. Other efforts have targeted fossil fuel or retail power price subsidies, which can make it challenging for renewables to compete. Support across the region continues to grow for distributed generation, particularly as prices for PV equipment continue to sink. Typically, these have taken the form of new net metering and investment subsidies.

Nonetheless, there continue to be significant obstacles to clean energy’s long-term growth in Asia. Integration problems have led to severe episodes of curtailment, with generators suffering from lost associated revenue. The financial well-being of local utilities (power distribution companies) continues to be in doubt, posing credit risks for developers looking to bring new projects on line. Finally, there are subsidies for retail electricity or fossil fuels. These are politically difficult to remove and can fundamentally undermine the economics of renewables.

RENEWABLE ENERGY CAPACITY GROWTH IS UNEVEN

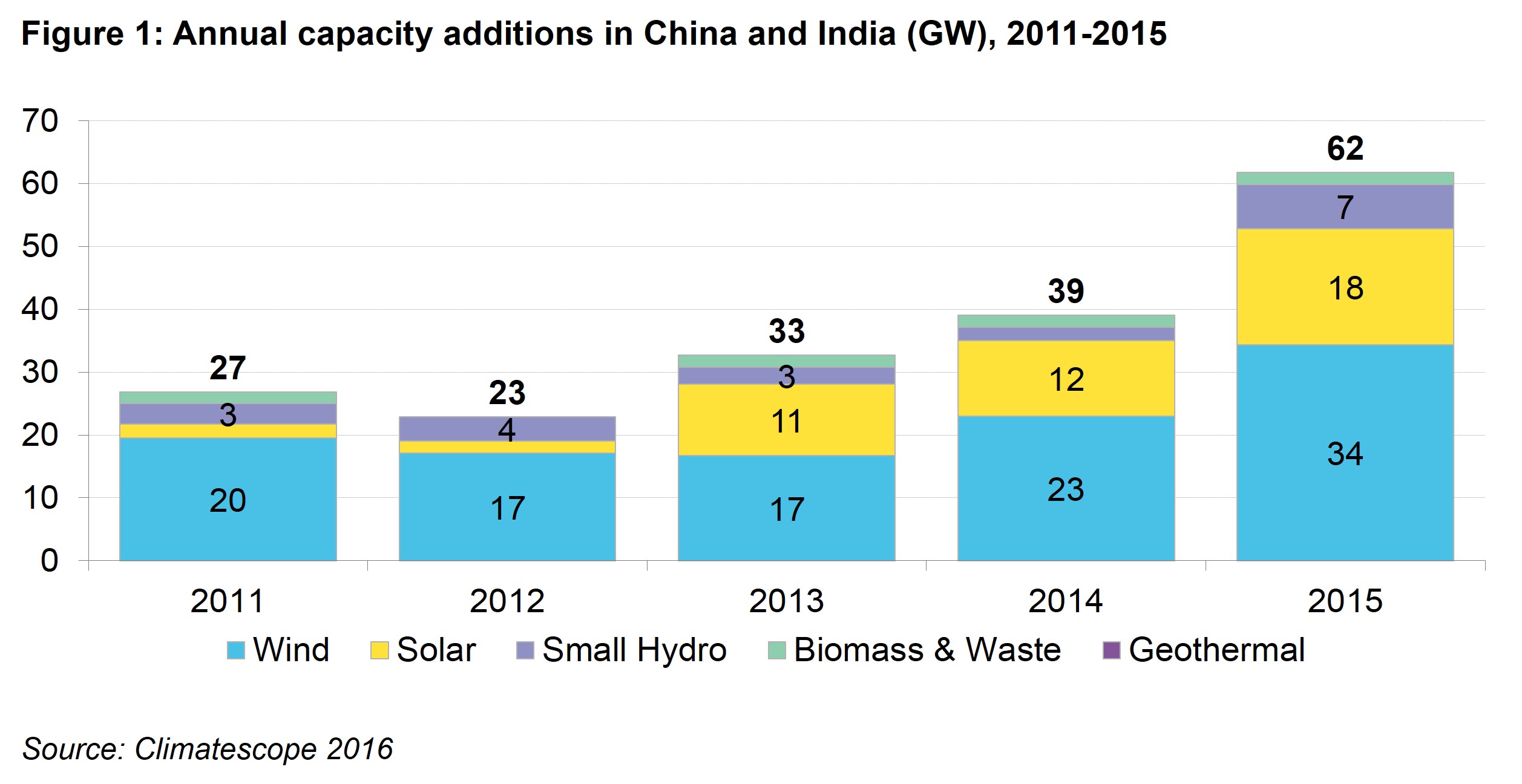

In 2015, Asian nations surveyed in Climatescope set an annual record for new clean energy capacity added. No less than 62GW of wind, solar, small hydro and biomass plants were commissioned during the year – up 60% from 2014. Today, these countries are home to 308GW of renewable energy capacity (excluding large hydro), equivalent to France and Germany’s combined total installed capacity.

Still, deployment has been unevenly split across the region. China, the world’s second biggest economy, has embarked on what is by far the largest renewables deployment programme in history. It accounted for 90% of the region’s new clean energy generation capacity installed in 2015. India was a distant second with 9% (5.6GW), mostly from wind and solar plants. China and India have seen renewable energy capacity installations grow every year since 2013, with onshore wind representing the bulk of the activity but solar accelerating recently (Figure 1).

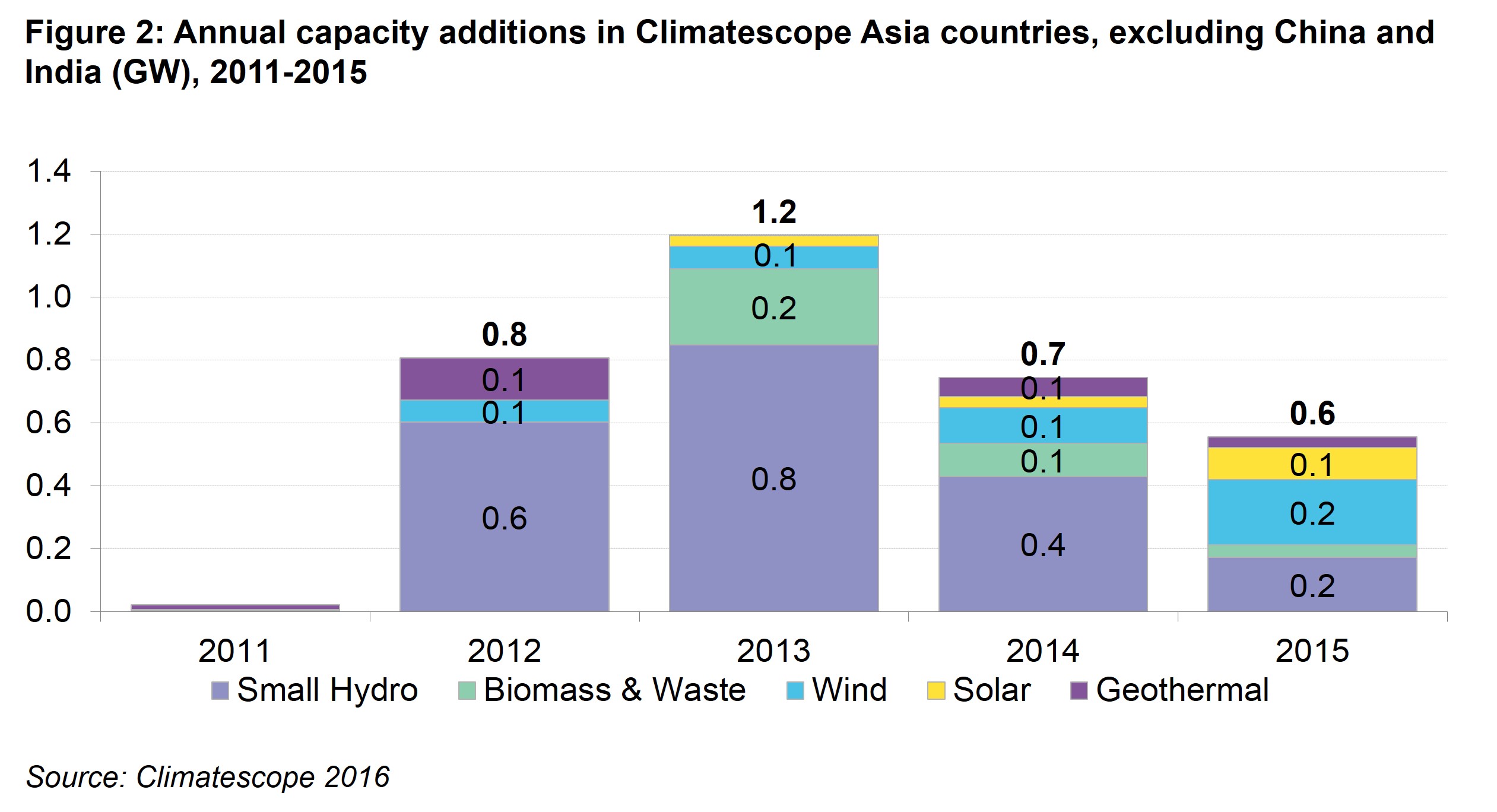

Installations in the rest of the Asian countries reviewed by Climatescope have been more irregular, although total new solar and wind have grown each year since 2011 (Figure 2). Pakistan saw the biggest uptick in 2015, with 758MW of mostly wind and solar, approximately five times what got built the prior year. Further deployment is set to continue thanks to new support made available by the Pakistani government in 2015, some of which is supported by China.

Vietnam and Tajikistan doubled their small hydro capacity from 2010 to 2015 while Sri Lanka and Nepal increased theirs by around a third. Finally, Nepal and Bangladesh have made important progress in off-grid clean energy. This is not accounted for in Figure 2, which shows only utility-scale activity.

INVESTMENT IS SPREADING TO PAKISTAN

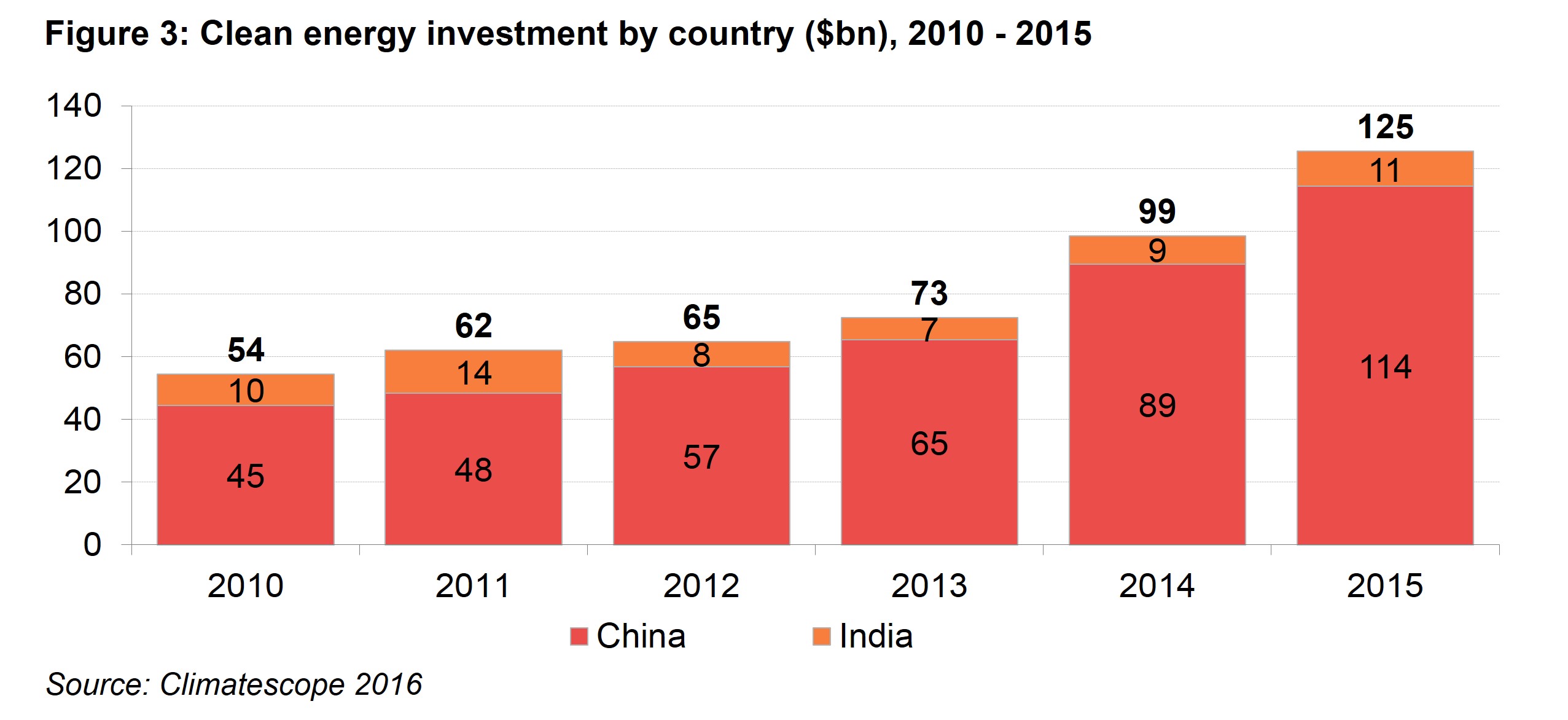

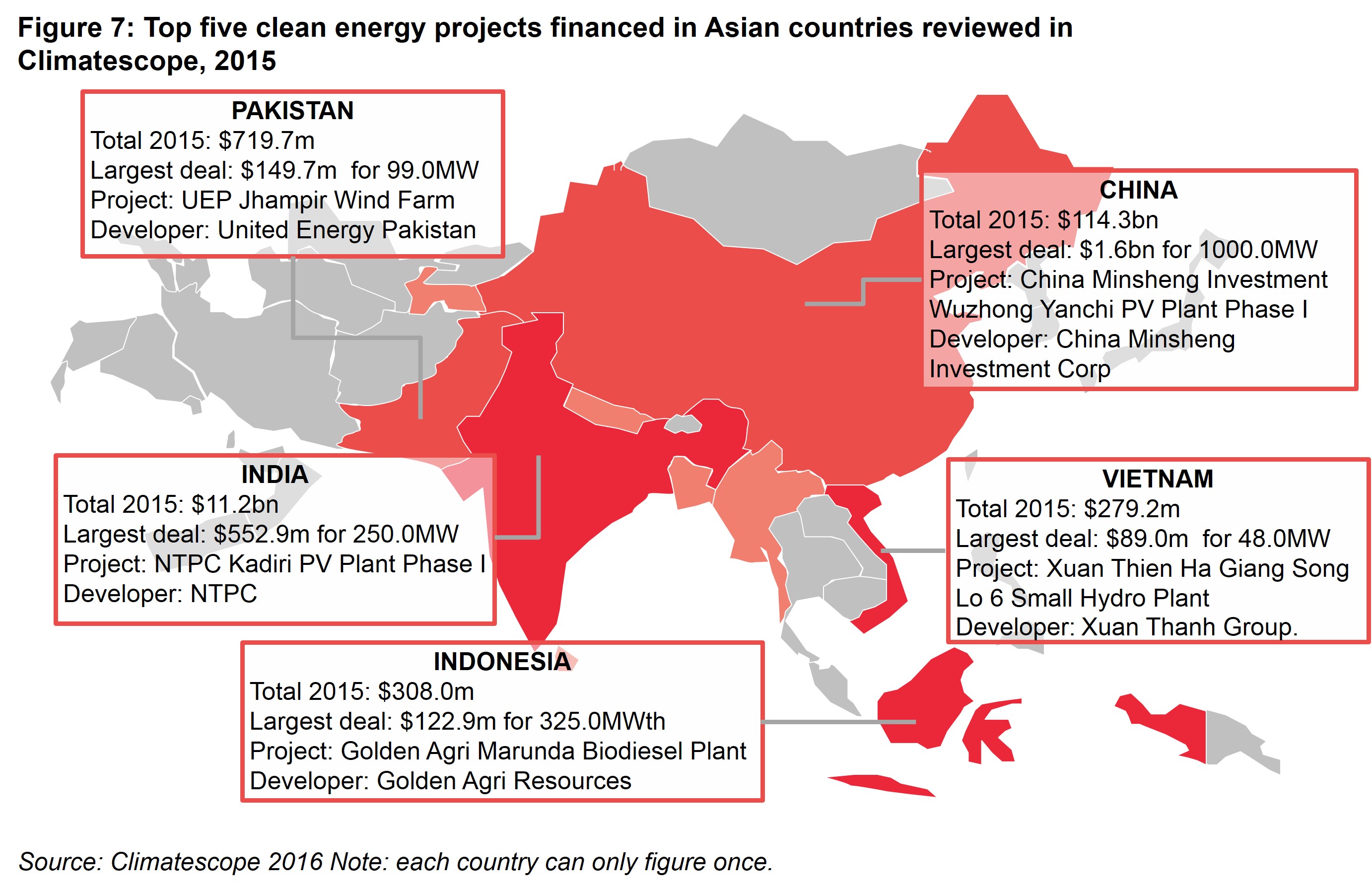

In 2015, the Climatescope Asia countries secured $127bn in clean energy investment, or 82% that deployed in all the 58 nations surveyed. Asia is the only region where investment has grown every year since 2011.

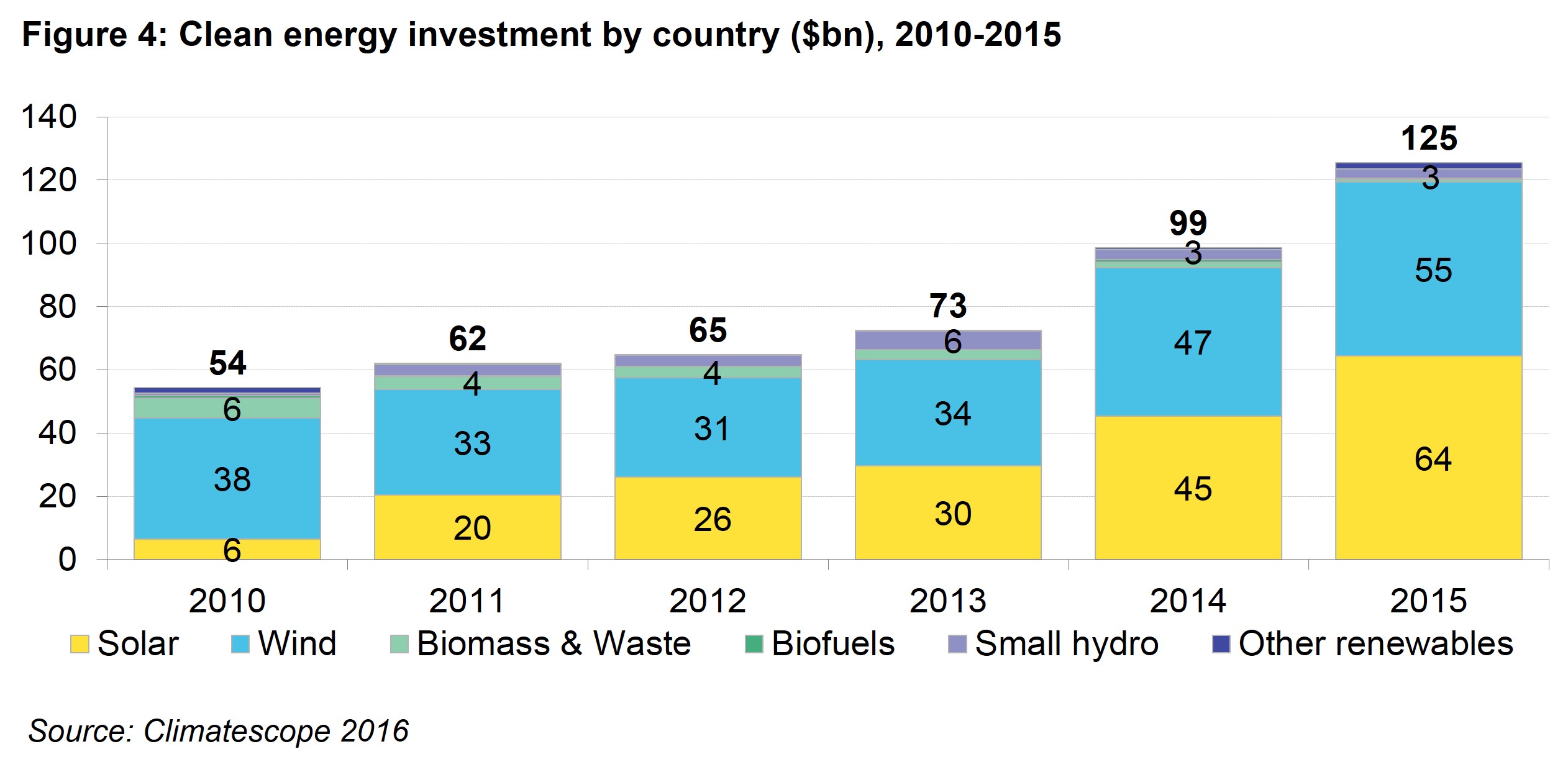

China and India in 2015 remained the first and second largest renewable energy investment destinations, respectively, and continued to see capital flows grow (Figure 3). For the first time, solar surpassed wind, attracting $64bn, or just over half of total investment. Bioenergy and small hydro have seen their shares shrink in recent years and accounted for a combined $6bn in 2015 (Figure 4).

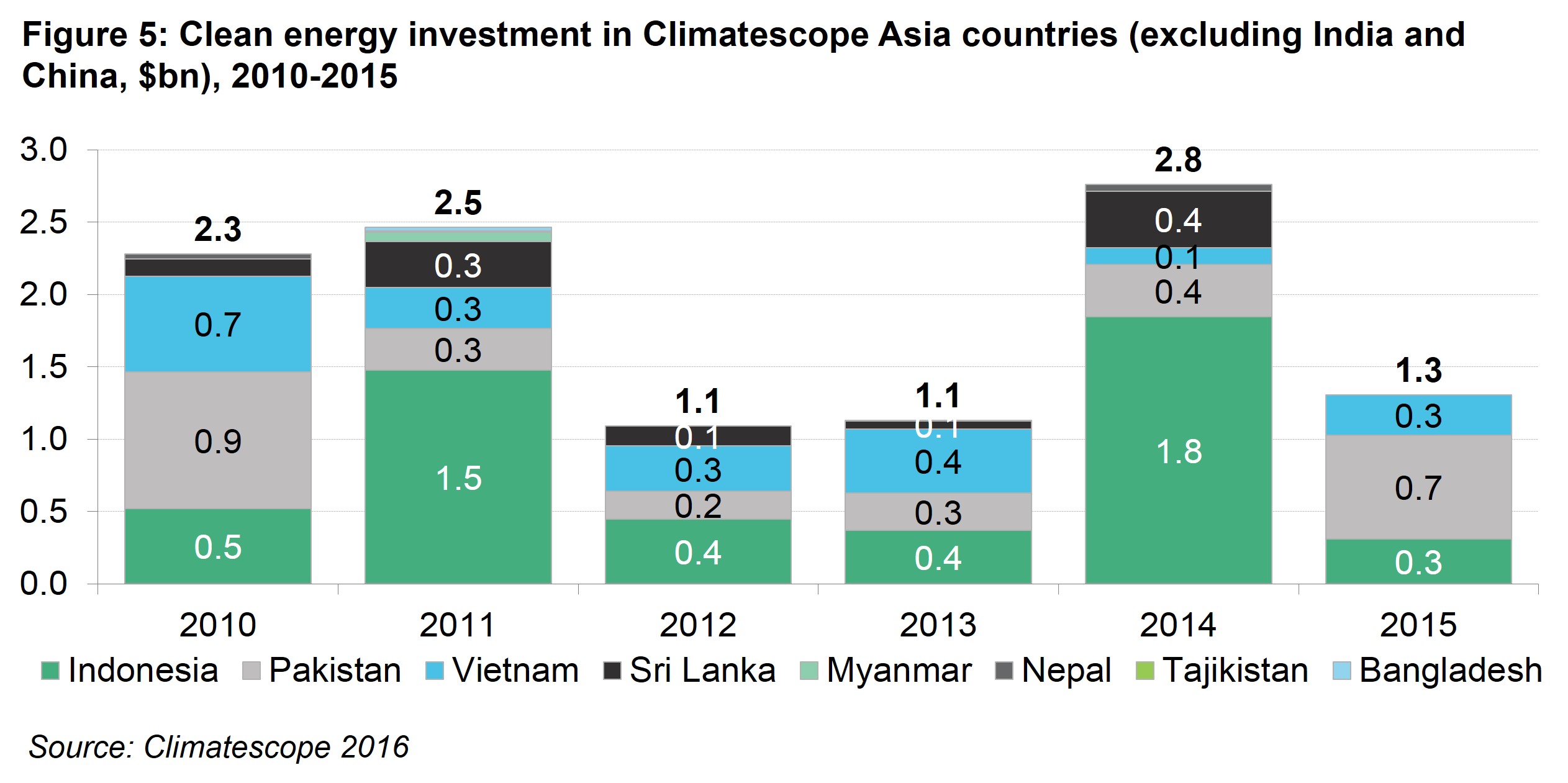

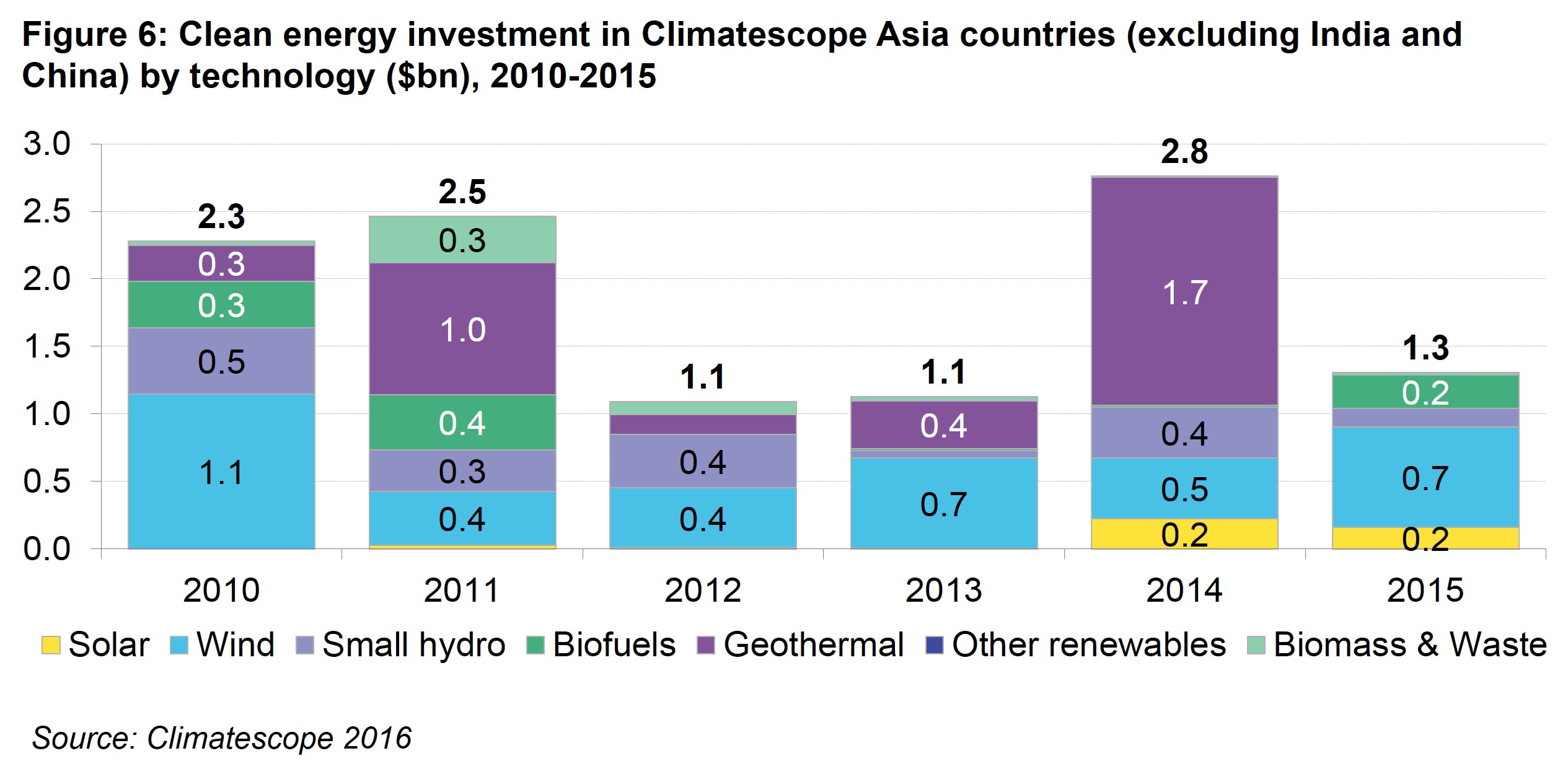

Away from India and China, other Asian nations saw a stark drop in investment, notably in geothermal projects. Total capital deployed in renewables in these countries fell by more than half, from $2.8bn to $1.3bn (Figure 5 and Figure 6).

Pakistan and Vietnam continued to raise their profiles with investors in 2015. Capital deployed doubled from $360m to $719m in Pakistan. In Vietnam, investment spiked to $280m in 2015 from $91m the prior year.

Indonesia’s, which had one of the highest levels of investment across all Climatescope countries in 2014, with $1.8bn, slipped to $308m in 2015. Indonesia’s headline figure was substantially boosted in 2014 by the $1.6bn Chevron Gunung Salak 330MW geothermal plant.

On the technology front in 2015, once again solar struggled to exceed 200MW installed in non-China/India Climatescope Asia nations (Figure 6). However, the spread of projects has improved. In 2014, some 98% of solar PV project financings occurred in Pakistan. In 2015, Pakistan still led with just over half of investments in solar but Vietnam took a third and Indonesia’s the rest. Vietnam and Pakistan are the only countries in which onshore wind projects were financed, confirming their leading role in this sector amongst this sub-group of Climatescope Asia countries. Other countries in the region saw no financings of utility-scale assets in 2015; however, Nepaland Bangladesh continue to have activity in off-grid renewables.

POLICY FRAMEWORKS EVOLVE IN FAVOUR OF RENEWABLES OR THEIR INTEGRATION

Asian Climatescope economies are more heterogeneous than those in other regions, with some clearly “middle-income” and others still struggling with the most basic energy access issues. What they shared in 2015 was a growing commitment to renewables.

Most adopted more ambitious renewables targets over the course of the year. Others, such as Bangladesh and Indonesia’s, were unsatisfied with their first attempts at competitive tenders and reverted to using feed-in tariffs to support clean energy. Still others, including China, are moving in the opposite direction and plan to hold further auctions in coming months.

MORE AMBITIOUS TARGETS FOR RENEWABLES, EMISSIONS

Four of Climatescope’s Asia countries ratcheted their renewables targets up in 2015 or are now in the process of doing so. India adopted the extremely ambitious goal of installing 175GW of renewables by 2022, including 100GW of solar PV. The Vietnamese government presented a more modest rise in its renewable generation target from 4.5% of generation to 6.5% by 2020, primarily to be achieved through solar PV. The target includes 850MW capacity by 2020 and 12GW by 2030. Bangladesh raised its renewable energy capacity target from 2GW to 3.1GW by 2020 with the aim of having renewables account for 10% of total capacity. Finally, Tajikistan’s government approved a new renewable energy programme for 2016-2020 that includes over 63MW of small-hydro projects and 4.3MW of solar to be built over the next five years.

Growing policy ambition on renewables was paired with new greenhouse gas (GHG) emissions reduction commitments made by all Climatescope Asia countries ahead of the UNFCC-organized climate talks in December 2015. China and India, which accounted for 30% of 2012 global GHG emissions and are expected to see the highest absolute CO2 growth of all countries in coming years, ultimately played a critical role in the signing of the Paris accord. China pledged to cut the emissions intensity of its GDP by 60-65% against 2005 levels by 2030, and India by 33-35%.

MIXED EXPERIENCES WITH CLEAN ENERGY AUCTIONS

In 2004, China became the first country in the world to use competitive tenders on a large scale as part of its renewable energy policy regime (well ahead of Brazil’s first renewables-specific auction in 2007). China used the auction to contract a sample of onshore wind projects ranging from 200MW to 1GW to establish the feed-in tariff that would be applied to the wider industry. The tariffs set started at $67.2/MWh (CNY 469) in 2003, bottomed out at $66.9/MWh (CNY 448) in 2006, and rose again to $78.2/MWh (CNY 515) in 2007, the year of the last auction.

Feed-in tariffs for wind and solar have since been used to allow China to become the world’s largest demand market for both technologies. Now, China is poised to return to using auctions, this time in a much wider manner to minimise costs while maximising growth. The government rolled out plans in June 2016 for more extensive tenders, starting with the solar PV sector.

Separately, conditions for non-regulated power generators have improved in China. The country now allows consumers to sign direct power purchase agreements with clean power projects. Meanwhile, renewable portfolio standards have been set for utilities across all of China’s provinces, with the first targets of 5-13% to be met in 2020.

China’s newest efforts on tenders follows in the steps of India, where the federal and state auction programmes have led to the largest competitive procurement of solar PV capacity anywhere. The country’s National Solar Mission alone awarded over 5GW of solar PV capacity contracts between 2013 and 2016, and the government recently set the extremely ambitious target of 100GW of solar PV installed by 2022, up from 4.4GW in 2015.

India’s government is now looking to replicate the successes enjoyed in PV with onshore wind, with around 10GW of new capacity to be auctioned between 2016 and 2019. The feed-in tariff that is currently supporting onshore wind and varies from state to state will continue in parallel. Finally, state-level renewable portfolio standards are under review, with the possibility of ratcheting up their 2019 goals.

The transition towards market-based mechanisms and the competitive procurement of renewables is less clear in the smaller Asian nations examined by Climatescope. Indonesia introduced its first solar PV feed-in tariff only in 2016 and is targeting just 250MW of new capacity following a complicated experience with tenders in 2013. Participants challenged the results of that reverse auction on the basis that bidding requirements and local-content regulations were set unfairly. Bangladesh’s tender programme on the other hand generated insufficient interest with around 150MW of projects contracted to date against a 500MW target in the pipeline.

BRIGHTER CONDITIONS FOR RENEWABLE ENERGY PROJECT DEVELOPERS

Lack of readily available capital and the risks associated with shaky off-takers are two challenges that have consistently plagued clean energy developers in emerging markets. But 2015 saw financial institutions and governments taking steps to mitigate both.

The Indian central bank added the renewable energy sector to its “priority” list in its lending guidelines to commercial banks. This in turn led to a reduction in its lending rate to commercial banks from 8% to 6.75% from 2014 to 2015 for funds earmarked for renewables. In Pakistan, the central bank made similar efforts specifically to help renewables by mandating commercial banks to provide developers of renewable power projects smaller than 10MW with debt at a fixed rate of 6% in 2015, down from 7.5% in 2014.

These efforts have been paired with measures to reduce off-taker risk. The federal government of India, for instance, has launched a debt restructuring scheme to cut operational losses at the country’s state-level power distribution companies (“discoms”). The scheme will also improve their solvency, and ensure portions of their cash flows are ring-fenced specifically to compensate renewables project owners for the power they generate.

Tajikistan has released a new energy sector strategy that calls for the restructuring of state-owned utility Barqi Tojik (BT) and seeks to address the deficit that has accumulated in the energy sector from selling electricity to consumers at prices that are not reflective of cost. Indonesia and Vietnam also took steps to reduce tariff deficits by phasing out some fossil fuel subsidies with an eye toward creating a more level playing field for renewables.

Finally, Indonesia has focused on cutting red tape that has slowed project development by moving all permitting processes to a “one-stop shop” in an agency set up by the ministry.

GROWING SUPPORT FOR DISTRIBUTED POWER GENERATION

India and Pakistan have joined Bangladesh and Nepal in supporting distributed renewable energy with an eye toward boosting energy access. Almost all major Indian states had adopted net-metering policies by the end of 2015, and the federal government reinstated a 30% investment subsidy for solar rooftop systems installed by residential and institutional consumers such as schools, colleges and hospitals. In September 2015, Pakistan approved net metering regulations to allow domestic, commercial and industrial owners of distributed solar and wind to sell surpluses generated back to the grid.

GRID CURTAILMENT, SUBSIDY PAYMENT DELAYS, AND OTHER CONTINUING CHALLENGES

Despite clear progress on certain areas, other challenges continue to plague clean energy in the Asian context. These include curtailment of production from certain renewables projects and non-payment by governments or utilities of certain subsidies.

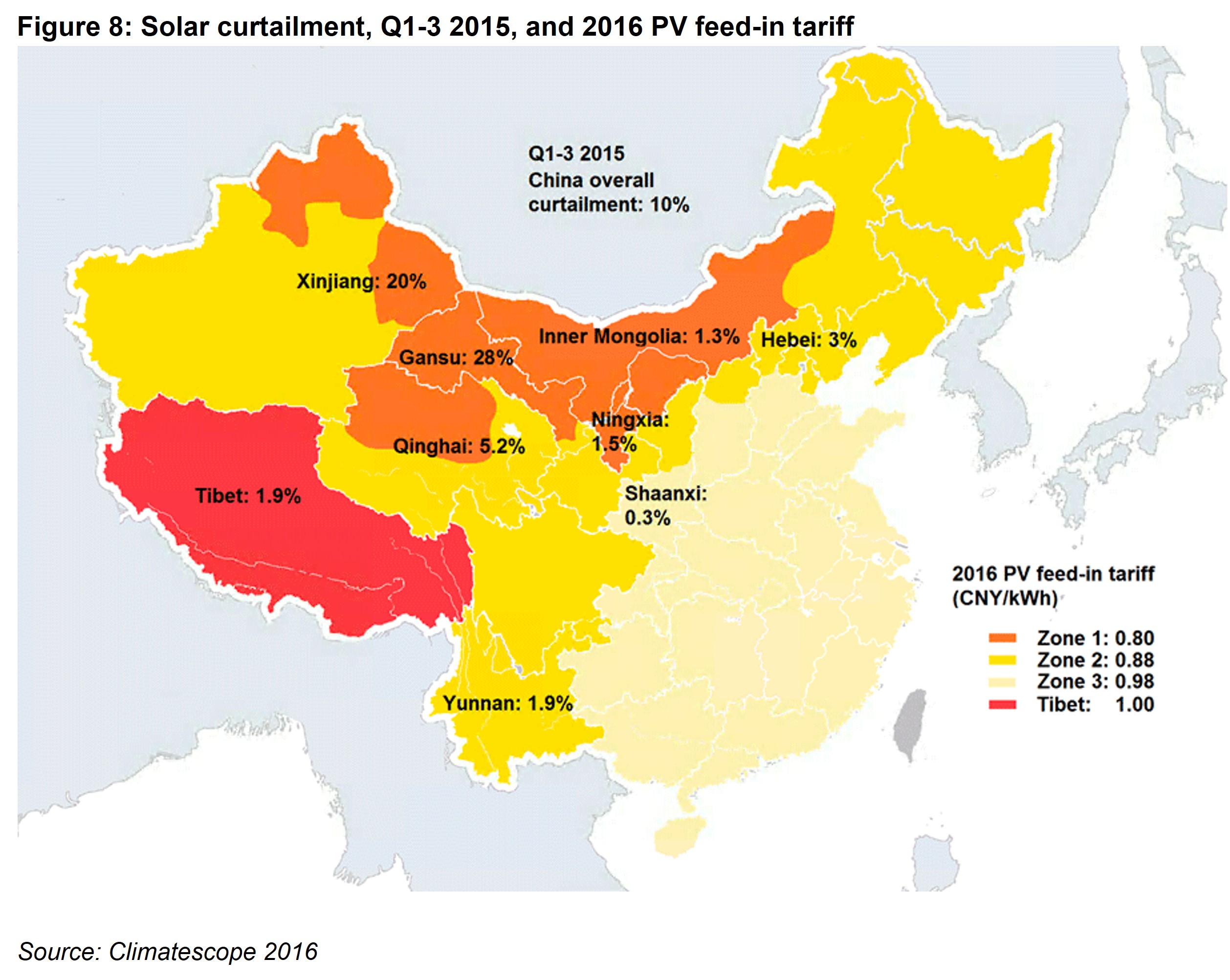

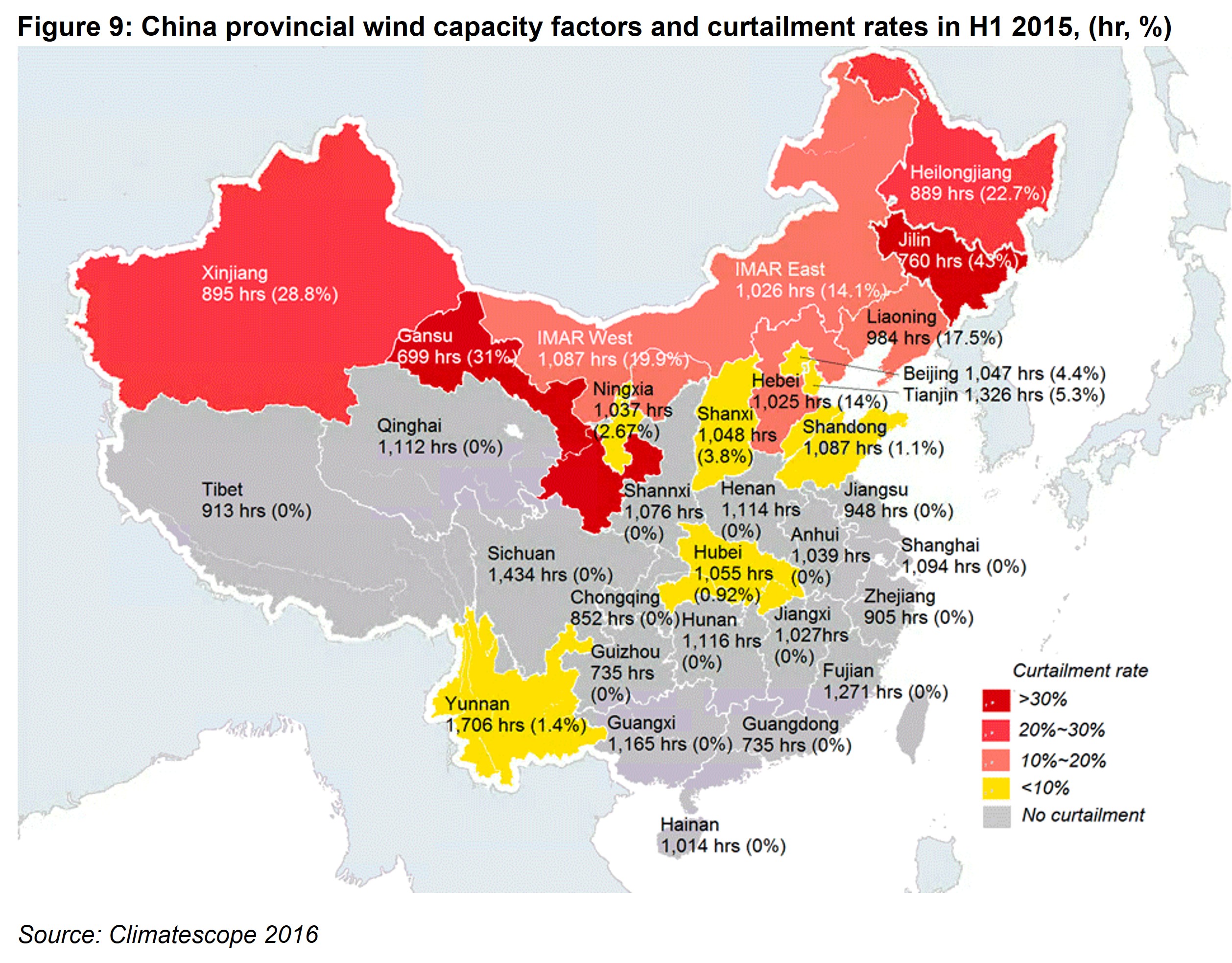

Grid curtailment of renewable energy in China became more severe in 2015 (Figure 8 and Figure 9). In western provinces such as Gansu, 39% of wind power and 31% of solar PV generation never reached consumers for use. Legislation drafted in 2005 that would clearly prioritize renewables on the wires over fossil-fuelled power remains to be implemented. In what appeared to be progress in 2015, the federal government said utilities would be required to dispatch minimum volumes of renewable energy. However, it remains unclear how this will be enforced.

Curtailment woes have been compounded by subsidy payment delays. As of end-2015, the Chinese government owed solar and wind developers a cumulative subsidy payment of $8.2bn, with some developers awaiting arrears of more than three years.

Development of long-distance transmission infrastructure to reduce curtailment risk is going full steam ahead in China and represents a definite bright spot for renewables project owners. China says it plans to invest $270bn in such infrastructure over the coming years, including in 11 new ultra-high voltage lines, many of which are already under construction. This is by far the most ambitious programme of its sort in the world and stands to have a transformative effect on the country’s power system and its economy more broadly.

The first signs of solar curtailment have started to emerge in India, particularly in the state of Tamil Nadu. Seeking to address the problems and preventing more from emerging, India’s federal energy ministry has asked central and state electricity regulators to award a must-run status for all solar and wind power plants in the country. However, this has proved ineffective thus far as local officials have largely avoided the edict. As of 2016, the Indian government has started considering additional regulations such as penalties for utilities that fail to prioritize zero-carbon energy.

The poor financial positions of utilities in some Indian states has also led to delays in payments to generators for power delivered. Onshore wind developers specifically have suffered through up to one-year delays in payments in the states of Maharashtra, Madhya Pradesh and Rajasthan. Some state utilities have also delayed signing power purchase agreements with new wind projects that are ready to be connected to the grid.

That said, the government’s debt restructuring programme is starting to deliver results. Some distribution companies are showing clear signs of repairing their balance sheets. Unfortunately, the financial problems for the discoms run deeper. Poor payment recovery and operational losses caused by subsidized retail electricity are likely to plague these companies for years to come, unless major reform is undertaken.

These structural challenges in China and India will need to be addressed if clean energy deployment is to continue at the pace seen in recent years. Between them, the two countries have 342GW and 30.5GW of new solar and wind capacity under development for which the power system will need to make space. The challenge is all the larger given that many of these projects are due to get built in the very areas that today are seeing significant curtailment.

Other utilities in the region will also need to review their balance sheets to accommodate future growth in electricity generation from renewables and other technologies. Off-takers in Nepal, Vietnam and Indonesia have all shown signs of financial weakness in recent years.

VALUE CHAIN EXPANSION MOVES SOUTH

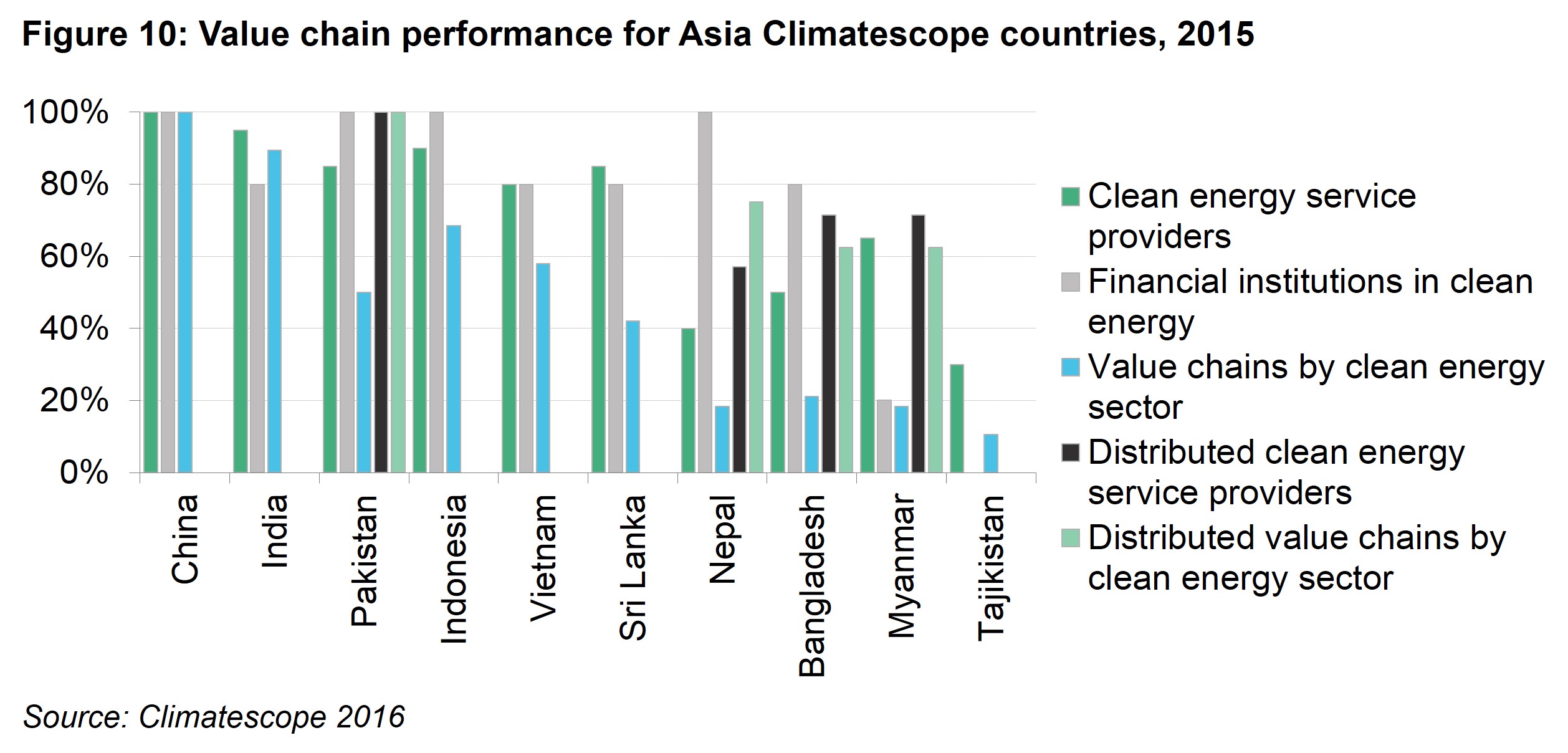

Asia as a region has become the world’s manufacturing hub, a fact reflected in Climatescope’s clean energy value chain scores. The region widened its lead over the other two surveyed on Parameter III with an average score across all Asian nations surveyed of 3.32. That marked a 0.09 improvement from Climatescope 2015 (Figure 10).

This change was largely due to supply chain expansion in India and Vietnam. China continues to achieve maximum scores for having the most complete renewables value chain amongst all Climatescope countries. As China’s supply chain matures and labor costs in the country rise, international companies are relocating production lines to South and Southeast Asia. Chinese-owned companies themselves are also expanding abroad, choosing South and Southeast Asia as first locations for overseas manufacturing.

Other value chain enhancements came from the number of venture capital and funds specialising in clean energy companies and projects in Indonesia, Bangladesh and Nepal.

Average scores

- %% region.name %%

- %% region.score[0].mean | round:2 %%

| Regional rank | Global rank | Country | Global score | Trend | Topics: 0.0 - 5.0 | Grid |

|---|---|---|---|---|---|---|

| %% country.score[0].regional_ranking | leadingZero:2 %% | %% country.score[0].overall_ranking | leadingZero:2 %% | %% country.name %% States | %% country.score[0].value | thousands:2 %% |

|

%% country.grid %% |